Plaid vs. DocGenie: asset summaries are not statements

Plaid is the right choice for engineering teams building fintech apps. For bookkeepers reconciling, paralegals tracing, or attorneys filing: Plaid will fail in a way that is not obvious from the marketing site. Here is where.

If you’re an engineering team building a fintech app, Plaid is almost certainly the right choice. We tell prospects this regularly. If you’re a bankruptcy paralegal, a divorce litigator, or a CPA reconciling a fund, Plaid will fail your use case in a way that is not obvious from the marketing site. This post is the version of that conversation we wish we could leave on every comparison page.

What Plaid actually delivers

Plaid is a data-aggregation API. Through a developer integration, it provides programmatic access to:

- Account-level data (balances, account names, masked numbers)

- Transaction history (date, amount, merchant string, normalized category)

- Identity data (account holder name, address, phone, when authorized)

- An “asset report”: a generated PDF summarizing balances and transactions over a window

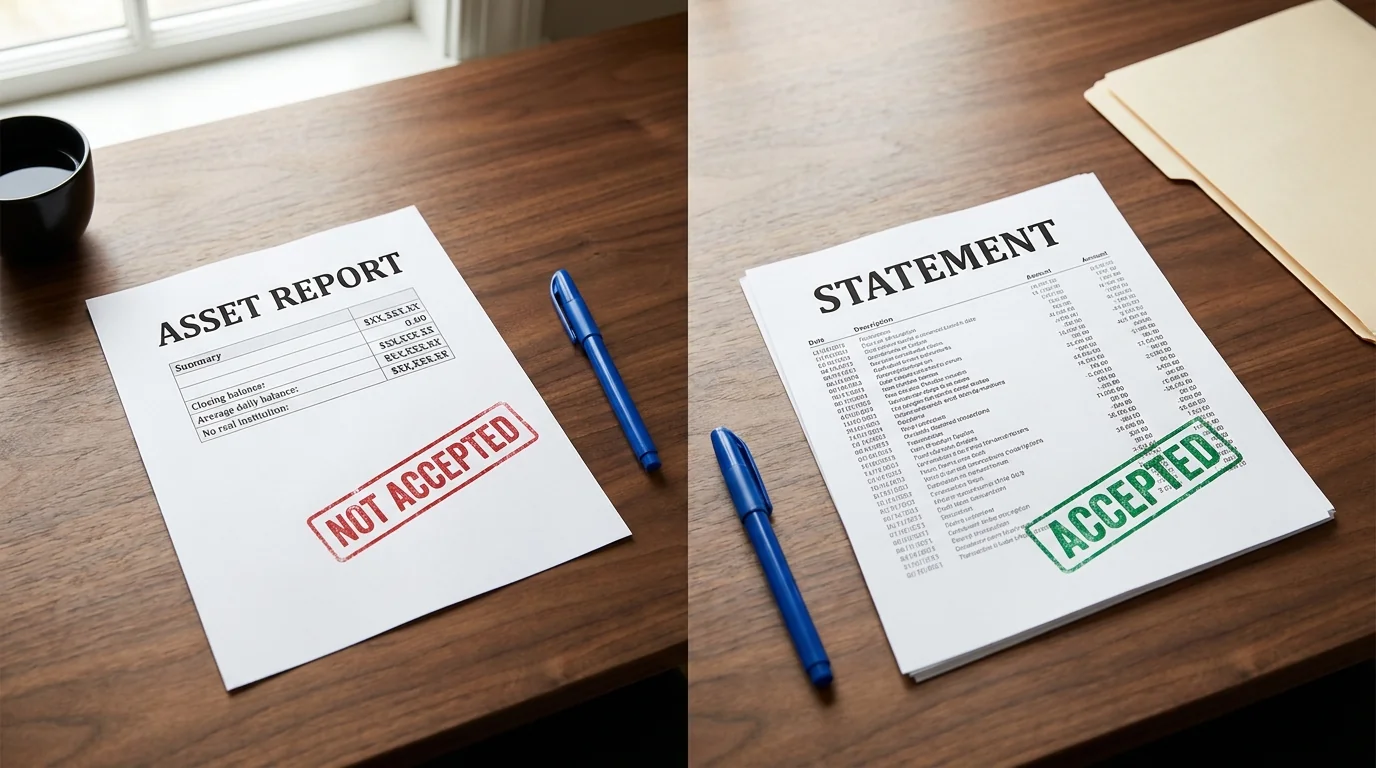

That last item is the one that gets confused in evaluation. The asset report PDF is generated by Plaid, not by the bank. It is a useful artifact for some lending workflows. It is not the institution’s statement.

“Plaid’s PDF is a summary about the account. The institution’s statement is the summary of the account. Different documents. Different uses. Different acceptability.”

Why courts won’t accept asset summaries

In consumer bankruptcy, the United States Trustee Program requires the petitioner to produce statements from each financial institution covering the months prior to filing. The statement is what the bank generates and signs. An aggregator’s summary is not a substitute. We have heard this verbatim from a managing partner at a 100-staff bankruptcy firm: a Plaid asset report came back marked unacceptable, and the team ended up doing manual retrieval after paying for the aggregation.

The same constraint applies in family-law discovery. Forensic accountants and tracing experts work from the institution’s actual statement, because the chain of custody runs through the bank, not through a third-party data aggregator. A summary that says “Plaid believes the closing balance was $X” is not what discovery production rules contemplate.

Why reconciliation requires the actual statement

Reconciliation is a comparison between two records: your books and the bank’s record of the period. The institution’s statement is the bank’s record. A transaction stream (Plaid’s, QBO’s, anyone’s) is a derivative produced by re-fetching, normalizing, and sometimes re-categorizing the data the bank exposes through its various endpoints. Derivatives are useful for daily operations. They are not the artifact you reconcile against, because by definition the derivative is one or more transformations away from the bank’s signed truth.

For a 30-client bookkeeping firm doing fund work, mortgage trust accounts, or anything regulated, this matters. When a third party (auditor, IRS, regulator, court) asks “show me the close,” the firm needs to produce the statement. Not the feed. Not the aggregator’s summary. The PDF the bank itself emitted.

The implementation gap

Plaid is engineering-required. It is, by design, an API for developers. To use Plaid, your firm needs to either:

- Build a Plaid integration, meaning hire or contract an engineer, write the OAuth flow, manage token refresh, handle institution-specific edge cases, and build the UI to expose the data to your team.

- Use a third-party tool that wraps Plaid and presents it as a no-code product, at which point you are now also dependent on that tool’s roadmap, pricing, and reliability.

For a non-engineering buyer (a CPA firm owner, a family-law administrator, a bankruptcy COO), option one is not available, and option two means evaluating tools where the underlying constraint (Plaid is a transaction feed, not a document feed) hasn’t gone away. We saw this happen in a sales call: a mortgage banker spent two months evaluating a Plaid-wrapped tool, then walked away when he learned a developer was still required to make it work for his pipeline.

The cost comparison

Plaid prices on API calls: typically per identity verification, per asset report, per linked account, with usage tiers. For a 30-client bookkeeping firm pulling 30 accounts × 12 statements/year = 360 retrievals, the API economics can be reasonable. For a 500-cases-per-month bankruptcy firm pulling 5,000 statements per month, the calls add up quickly.

DocGenie meters retrieval in credits: a statement runs one to five credits by retrieval depth, with most major US banks at the top of that range and premium connections (certain brokerages, multi-step utilities, custom institutions) costing more. The pricing aligns with what is actually expensive (the multi-aggregator backend that turns “give me the statement PDF for July 2025” into a working session at the bank). For high-volume retrieval, the credit model is usually cheaper. For low-volume retrieval, both are inexpensive.

| Plaid is right when | DocGenie is right when |

|---|---|

| You’re an engineering team | You’re a CPA, paralegal, or COO with no developer |

| You need transaction data, not documents | You need the institution’s actual statement PDF |

| An asset summary is acceptable to your downstream party | The court, auditor, or underwriter requires the bank’s signed document |

| You’re building a consumer fintech app | You’re running a firm with a recurring close |

| API integration is a feature, not a blocker | You need files to drop into Drive, OneDrive, or SharePoint today |

What we tell engineering teams

Plaid. Use it. Don’t waste a discovery call on us if your team is comfortable wiring the integration and your downstream consumer accepts asset-summary output. We are a no-code product for non-engineering buyers who specifically need source documents. That is a different category and a different sales motion.

The mistake on both sides is treating the categories as competitive. They’re complementary in the broader fintech-infrastructure stack. Plaid won the data layer. The document layer is open. We’re building it.

Closing

A summary is a summary. A statement is a statement. The difference shows up the first time a third party asks you to produce one and you produced the other. If your workflow has any step where the answer “the bank’s PDF” matters, do not use Plaid. If your workflow is transaction-data-only and your team includes engineers, do not use us.

Both products work, for the buyers each was built for. Pick on use case, not on category overlap.

Stop chasing this month's statements.

Free for 2 connections, 3 credits a month — enough to pull Amazon and Capital One every cycle. No card.